| Type of paper: | Research paper |

| Categories: | Unemployment Inflation |

| Pages: | 7 |

| Wordcount: | 1794 words |

In economics, inflation refers to the increase in the prices of goods and services in the economy. Unemployment, on the other hand, refers to the condition where no jobs exist but people are willing to work at the existing wage rates. In a business cycle, unemployment and inflation are critical issues. In fact, in any country, both unemployment and inflation are major performance indicators. As known, inflation affects the rate of unemployment in an existing economy. Policymakers have failed to deal with inflation and unemployment. When monetary and fiscal policymakers elongate the aggregate demand by and move upwards towards the aggregate supply curve, a shortage of employment opportunities exists, which eventually comes at a cost of demand-pull inflation. In economic terms, trade-offs exist between inflation and unemployment. Whenever there is lower unemployment, inflationary pressure on the economy exists. This paper provides an economic analysis of inflation and unemployment by using the concept of the Phillips Curve.

An Analysis of Unemployment and Inflation using the Phillips Curve

Phillips Curve researched the trade-offs between inflation and unemployment. Alisa (90) indicated that the Phillips Curve was sensibly very much affirmed by statistical indicators of various nations in 1950 - 1960s. Amid this time the economies of numerous nations accomplished the full employment (Alisa 90). In any case, the policy adoption went for the further expanding of production and diminishing joblessness, the ascent in costs has quickened, and the log jam in inflation was joined by increments in joblessness (Alisa 90). There are diverse clarifications of the presence of the reverse connection between inflation and unemployment. The author explained this issue partly with the role of flexibility in the labor market. In her explanation, Alisa (90) indicated that unless full employment exists in the economy, a few sectors of the labor market will stay unaltered unemployment, yet the circumstances on the other markets could prompt unsatisfied demand. This whole situation could prompt the greater expenses, development in wages thus more expensive rates. The macroeconomic consequence of this procedure will be accelerated inflation. The author added that the other clarification of the Phillips Curve is the undeniable actuality, that for producers and workers, it is simpler to increase prices and wages amid times of economic growth. They added that whenever they is high unemployment rates, people are forced to accept low wage which undeniably breaks inflation in regards to salary and prices. On the contrary circumstance, as full employment is achieved, there is a developing demand for extra factors of production (Alisa 90). The result of this circumstance can be that the growth in wages would outstrip the growth in productivity. That can prompt inflation in the prices and salary. The consequence of these procedures will be inflation. Indeed, the essence of the Phillips Curve is visually represented by analyzing the curves of supply and demand. The development of aggregate demand in the economy makes new irregular characteristics and mentally builds limited assets. Subsequently, it is evident that with the growth and demand, inflation is expanding. The bigger the increase in aggregate demand, the closer the economy is to have full employment, the more expensive rates will exist.

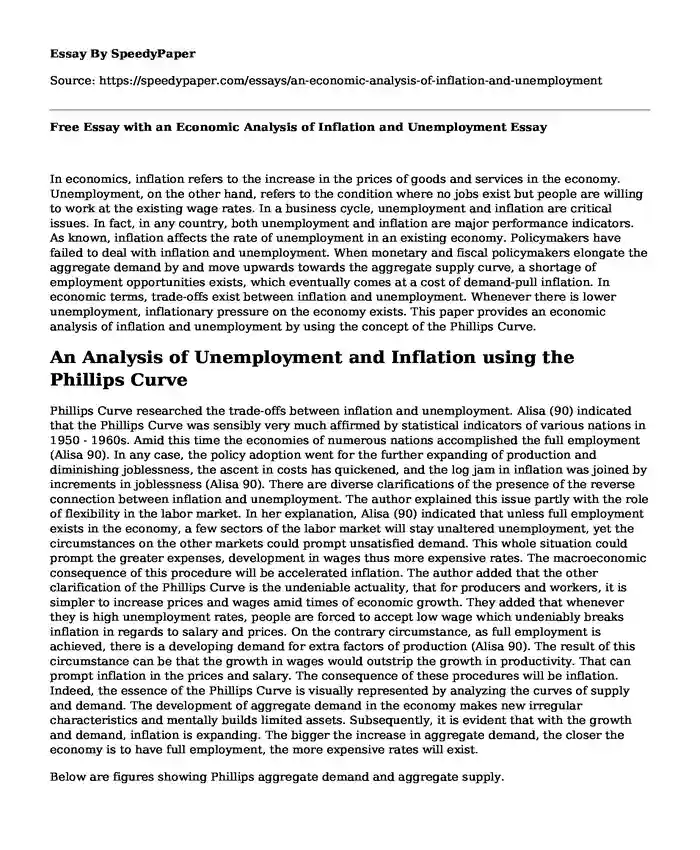

Below are figures showing Phillips aggregate demand and aggregate supply.

Inflation rate %

E'

E

Phillips Curve

0 Unemployment rate %

Price AS

E'

P2E

P1

AD2

AD1

Outputs Y

Inflation rate %

P2% E'

P1% E

Phillips Curve

U1 U2 Unemployment rate %

Discussion

Consider an economy which is right now in equilibrium at point E with Q1 dimension of output being delivered at value level P1. The present dimension of unemployment in the economy is u1 and the current inflation rate is winning at p1%. Assume because of the financial or money related approach, there is an expansion in the aggregate demand from AD1 to AD2 (rightwards move). In the short run, there is an expansion in the dimension of the output of goods and services from Q1 to Q2 and increment in the value level from P1 to P2. New equilibrium point for the economy with a more elevated amount of output and value level is found at E'. The Larger output implies a more elevated employment rate and, in this manner, a lower level of unemployment, u1 to u2. Higher price rate level methods a more elevated amount of inflation (p2%) in the economy. Subsequently, in the short run, the move in the aggregate demand curve influences inflation and unemployment rates in inverse ways.

Since monetary and fiscal policies can move the aggregate demand curve and influence the dimension of inflation and unemployment rate on the Phillips Curve, such strategies can be utilized by the policymakers to pick the ideal mix of unemployment and inflation. The increase in cash supply, increment in government spending or tax breaks extend the aggregate demand rightwards move of AD curve and consequently moves the economy on a point on the Phillips curve with lower unemployment and higher inflation rate. So also, a decline in cash supply, a decline in government spending or increments in duty rates prompts the constriction of aggregate demand leftwards move of AD curve and hence moves the economy on a point on the Phillips Curve with the higher unemployment rate and a lower rate of inflation.

Unemployment and Inflation in America

Blanchard (1) asserted that the US Phillips Curve is still existing but its current shape would bring future problems to monetary policy in the future. Furthermore, Michas (p.1) affirmed that the U.S. CPI and pay wage remains unobtrusive today, regardless of an almost eight-year U.S. monetary development and an unemployment rate that has just dipped under the Federal Reserve's assessed normal rate of unemployment. According to the author, this provides reason to feel ambiguous about the significance of work advertise slack as a driver of inflation. Similarly, the Fed has been efficiently limiting low market-based expansion desires, ascribing them to either diminished liquidity in the Treasury Inflation-Protected Securities (TIPS) markets or to changes in the inflation rate premium. The author added that the dispersion of potential inflation results and markets perception of the probability of drawback or upside misses. The most recent research from the European Central Bank (ECB) proposes that a negative inflation rate premium is related to deflation risks, as opposed to low inflation uncertainty (Michas, 1). Generally, the market doles out a higher likelihood to the Fed's absent to the downside. Meanwhile, the unemployment rate fell beneath the Fed's characteristic rate gauge in December 2016, which should in principle heighten upward weight on costs (Michas, 1). Rather, astoundingly feeble CPI prints in March and April brought the Fed's favored proportion of market-based long haul expansion desires down to 1.9%, around a large portion of a rate point beneath the Fed's objective in CPI terms. The April CPI report reflected expansive based shortcoming over a scope of center merchandise and ventures, provoking us to change our multi year-end PCE conjecture to 1.5%, versus the Federal Open Market Committee (FOMC) middle projection of 1.9% and its 2% PCE target (Michas, 1).

Kasseh (1) affirmed that the ramifications of the oil shocks which occurred amid the 1970's and 1980's is that in the event that OPEC should cut output and raise world costs of oil today, at that point there is a probability for certain economies to at the same time experience high inflation and unemployment, which may differentiate the general thought exhibited by the Phillips Curve. In such a circumstance, depending on the Phillips Curve for policy purposes and for strategy purposes will present genuine results (Kasseh 1). The certainty being that policymakers would be compelled to pick between fighting unemployment either by exhausting aggregate demand or diminishing inflation by packing aggregate demand. While this circumstance may put policymakers on in applying a Philip-based Curve for inflation forecast, a few investigations have presumed that the expanded inflation experienced by the U.S somewhere in the range of 1980s was because of profitability slowdown and furthermore policymakers finding out about the persevering exchange in inflation and unemployment (Kasseh 1). Different examinations have likewise demonstrated that the concurrent high inflation and unemployment was because of the way that, monetary policymakers worked with misspecified Phillips curve (Kasseh 1). This can be explained in the figures below

Price

AS2

AS1

P2 E'

P1E

0 Y2 Y1Output

Inflation rate %

P2%E'

P1%ESPRC2

SPRC1

0U1 U2 Unemployment rate %

Discussion

Based on the figures, we can take a look at an economy that operates at the equilibrium point E, and utilizes aggregate output Y1 at the aggregate cost stage of P1. Because a negative shock exists, the cost of production of companies rises, which makes the aggregate supply curve to shift towards the left from AS1 to AS2. The yields from the aggregate decline from Y1 to Y2 and the cost levels increase from P1 to P2. The falling output level, which is often referred to as stagnation combines with the rise in prices of services, which is inflation, to create what is known as stagflation.

To delve deeper, it is predetermined that when the yields of a firm begin to fall, the company begins to cut labor cost to enable the fewer workers to produce output. This situation creates unemployment in the economy. Furthermore, at P2, it is noticeable that the price level in the economy is high, which will cause the inflation rates to rise. Seemingly, when the aggregate supply curve shifts because of the increase in oil prices also referred to as the adverse shock, higher unemployment and higher inflation is witnessed. Due to that, short run Phillips Curve moves from SRPC1 to SRPC2. From the graph, the rate of unemployment rises from u1 to u2 and the rate of inflation rises from p1% to p2%.

Evidently, policymakers have a difficult time to deal with the supply shock. This is because the rate of unemployment and inflation is staggering making it difficult for them to fight the two variables. This can be seen in two ways. If they try to expand aggregate demand, the inflation rate will increase by a large margin. On the other hand, if they try to contract the aggregate demand, the unemployment rate would increase further as well.

Conclusion

Overall, the study provides an economic analysis of inflation and unemployment by using the Phillips Curve. From the analysis, it is determined that inflation and unemployment are key and critical indicators in a country. Besides that, research in the topic has revealed that there is a negative relationship between inflation and employment to economic growth. This means that unemployment and inflation affects the economic growth of a country. The Phillips Curve better explains the relationship between inflation, unemployment, and economic growth. It uses the labor force as its driving factor. There have been many studies, which have examined inflation and unemployment in various countries. However, this paper looked at the two variables in...

Cite this page

Free Essay with an Economic Analysis of Inflation and Unemployment. (2022, Feb 22). Retrieved from https://speedypaper.com/essays/an-economic-analysis-of-inflation-and-unemployment

Request Removal

If you are the original author of this essay and no longer wish to have it published on the SpeedyPaper website, please click below to request its removal:

- Essay Example on Dabbawala Service Organization

- Essay Sample on Social Networking in Automotive Technology

- Scholarship Cover Letter Sample in Our Free Essay

- An Essay Sample about Ethics in Sports

- Why Are Americans Rapidly Becoming More Obese? Free Essay

- Free Essay: Summary of the Development of the Behavioral Matrix

- Article Analysis Essay: ERPs Reveal Differences In Syntactic Processing

Popular categories