| Type of paper: | Essay |

| Categories: | Management Finance Thesis |

| Pages: | 4 |

| Wordcount: | 1032 words |

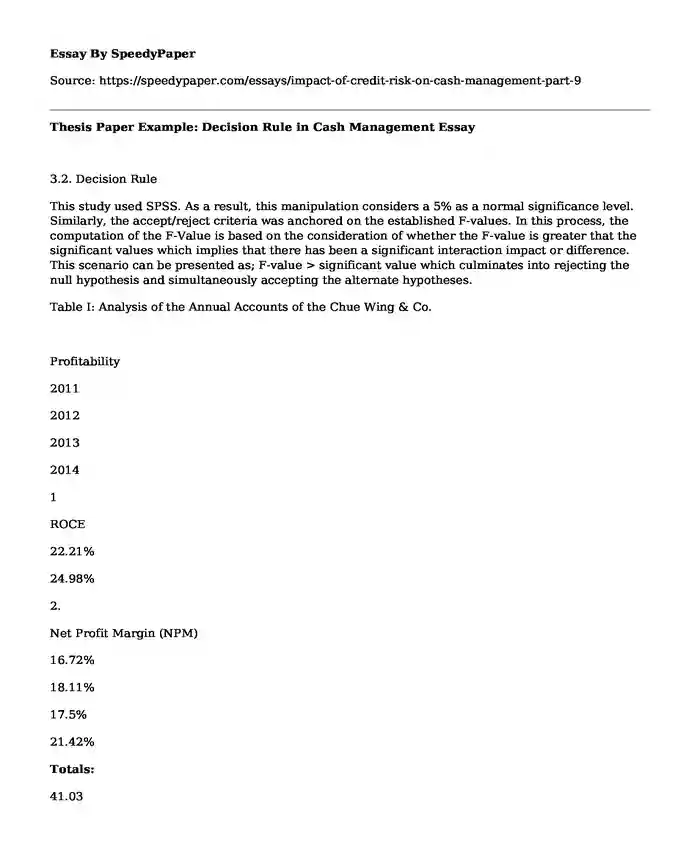

3.2. Decision Rule

This study used SPSS. As a result, this manipulation considers a 5% as a normal significance level. Similarly, the accept/reject criteria was anchored on the established F-values. In this process, the computation of the F-Value is based on the consideration of whether the F-value is greater that the significant values which implies that there has been a significant interaction impact or difference. This scenario can be presented as; F-value > significant value which culminates into rejecting the null hypothesis and simultaneously accepting the alternate hypotheses.

Table I: Analysis of the Annual Accounts of the Chue Wing & Co.

Profitability

2011

2012

2013

2014

1

ROCE

22.21%

24.98%

2.

Net Profit Margin (NPM)

16.72%

18.11%

17.5%

21.42%

Totals:

41.03

20.25

40.32

46.4

Liquidity

3

Credit Payment Period (CPP)

102.3

157.14

141.33

179.34

4

Debtors Collection Period (DCP)

98.5

101

96

122.5

Totals:

200.8

258.14

237.33

301.84

Source: (Chue Wing & Co. financial reports 2011, 2012, 2013 and 2014).

Table II: Analysis of the Annual financials of Oriental Foods Company Limited

Profitability

2011

2012

2013

2014

1.

Net Profit Margin (NPM)

37.24

41.67

48.34

2.

ROCE

24.9

29.78

28.25

32.21

Totals:

62.89

67.02

69.92

80.55

Liquidity

3

Credit Payment Period (CPP)

62.45

74.10

77.25

78.65

4

Debtors Collection Period (DCP)

31.34

43.12

34.53

46.11

Totals:

93.79

117.22

111.78

124.76

Source: (Oriental Foods Company Limited financial report 2011,2012,2013 and 2014)

Table III: Analysis of the Annual financials of Yoma Strategic Holdings Company

Profitability

2011

2012

2013

2014

1.

Net Profit Margin (NPM)

2.02

4.50

3.60

2.

ROCE

1.66

4.60

4.05

Totals:

3.68

9.10

7.65

11.84

Liquidity

3

Credit Payment Period (CPP)

62.54

69.32

73.45

79.05

4

Debtors Collection Period (DCP)

67.11

73

95.67

97.98

Totals:

129.65

142,32

169.12

177.03

Source: (Yoma Strategic Holdings Company financial report 2011,2012,2013,2014)

The impact of the credit policy on the cash management capacity of the three companies was also a major basis for the evaluation of the profitability nature and perspective of the companies both in the short-run and in the long-run. In particular, the four years span provides the basis for the projection of future performance matrix of the companies which is essential for leveraging cash management portfolio and the entire investment decision. In this regard, the hypothesis identified above was subjected to test in order to determine the impacts of credit policies on profitability of the FMCG divisions of the ABC Group of companies. The main factor of consideration is the analysis of the trend pertaining to the performance of the companies over a span of four year (2011-2014).

The two sets of hypothesis as stated in the earlier section were subjected to Analysis of Variance (ANOVA) to test their applicability and viability as shown below:

To test the first Hypothesis:

Ho: Credit policy can influence profitability managements in the FMCG sector of ABC Group of Companies

From the above model, the dependent variable is the level of profitability of the FMCG companies of ABC Group while the predicting variable is the credit policy.

Decision Making: from the above literature, if the F-values is equivalent to or larger than the significant value, then, it implies that the null hypothesis does not hold hence, rejected while at the same time accepting the alternative hypothesis. From the above model, the F-value is larger than the significant value given that (8.231> 0.564). Therefore the alternative hypothesis does not hold hence discarded while accepting the null hypothesis that stated: Credit policy can influence profitability managements in the FMCG sector of ABC Group Companies

Testing Second Hypothesis: ANOVA

Ho: There is a remarkable correlation between debtors turnover of the three FMCG Companies and their liquidity position:

Table V: ANOVA for Hypothesis 2

Model used

Sum of the Squares

Difference (df)

Means Squares

F-Values

Significance (Sig)

Regression

892.45

1

892.45

0.765

0.267

Residual Values

1383.50

1

1383.50

Totals

13,941.58

2

From the above analysis, the dependent variable is the liquidity management while the predictors that assist in decision making and the determination of the implication of the hypothesis is the credit grant. In this regard, any time the F-value is bigger than the significant value, the null hypothesis is rejected while the alternative hypothesis is accepted. In the above ANOVA, the F-values is larger than the significant values given than 0.765 is greater than 0.267. Therefore, the alternative hypothesis was rejected and the null hypothesis accepted. The null hypothesis stated that, there is a significant relationship between the liquidity position and the debtors turnover of FMCG companies of the FMCG companies in ABC Group. This is an important assertion that is used to inform the impact of debtors turnover and their liquidity positions in the activity pertaining to cash management of the Fast Moving Consumer Goods companies of the ABC Group. The analysis is based on the implications of the data obtained from the financial reports of the companies over a span of 4 years (2011-2014).

3.3. Analysis of Cash Conversion Cycle (CCC)

The cash conversion cycle provides a metric measure that is used to evaluate effectiveness of the management of companies as well as the overall financial health of the business. It measures the speed at which companies are able to convert cash on the hand to inventories as well as accounts payables via sales and accounts receivable and back to cash. With regard to this aspects, in 2011, the accounts that had been held with the central depository as cash inventory for Chue Wing & Co. had been RsM 282,588 while in 2012, and RsM 376,903 in 2014 the value had risen to RsM 299,487 while the average daily turnover changed from 41 to 54.7 and 79.3 in 2014. This was a lucrative change in the cash evolvement of the company thus demonstrating a potentially positive implication of the financial health of the company.

On the other hand, Yoma Strategic Holdings also demonstrated equally positive financial performance over the 4 years period despite the dynamics in the FMCG market segment. In particular, on average, between 2011 and 2014, the companys investments in real estate comprised of 44 percent of its entire investments and generated more than 90 percent of its revenues. For instance, in 2013, the companys current assets were $164,795, 000 which was a rise of 20 percent from 2012, 26.4 percent rise from 2011 and an expected rise of approximately 11.5 percent in 2014. This was quite remarkable through increase in cash inventory by virtue of the current assets.

Finally, Orient food performance also indicated reasonably poor propensity for future excellence with regard to cash conversion and the trend in profitability. For instance, one of the factors that demonstrate poor future performance includes the net cash flow that stood at RM 12,946,990 in 2011, RM 8,586,351 in 2012, 7,784,985 in 2013 and RM 8,674,945 in 2014. This trend was particularly worrying as the company had been simultaneously going through a period of progressive change over time and could eventually experience indefinite draw back on its investments products as its ability to manipulate working capital constrained immensely.

Cite this page

Thesis Paper Example: Decision Rule in Cash Management. (2017, Sep 10). Retrieved from https://speedypaper.com/essays/impact-of-credit-risk-on-cash-management-part-9

Request Removal

If you are the original author of this essay and no longer wish to have it published on the SpeedyPaper website, please click below to request its removal:

- Literary Essay Sample: Death of a Salesman vs The White Heron

- Theory of Knowledge Essay Sample

- Free Essay Sample on Customs and Language

- Free Essay: Manufacturing Depression, Causes of Depression and Treatment

- Free Essay Sample: Life Without Parole for Juveniles

- Aligning IT and Business Strategy, Free Essay Sample

- "Daddy" and "Lady Lazarus" - Free Essay Analyzing Sylvia Plath's Poems

Popular categories