| Type of paper: | Essay |

| Categories: | United States Finance Government |

| Pages: | 4 |

| Wordcount: | 928 words |

Alabama is a state in the South Eastern part of the US. It is the immediate neighbor of Tennessee and Georgia states with Mississippi to the Western part. This state is amongst the top 24 states with a high population of the 50 states of the US and has for long been identified as Yellow Hammer or the Heart of Dixie, ("Alabama Department of Finance-Executive Budget Office", 2016). The diversified agricultural practices have made this state peculiar in the economic growth pattern of the US states over time. It’s due to this that various departments such as healthcare, education, technology, manufacturing, aerospace and finance have substantially grown.

The distribution of income has been consistent on different sources for the past three years specified as 2013, 2014 and 2015. These include;

· Driver’s License fees which are collected by the department of Public safety

· Federal funds that are usually directed to education, healthcare, energy as well as other normal governmental operations.

· Corporation fees

· Contractors’ taxations on any construction within the state

· Produce levies on products such as tobacco and cigarette. This is usually done on the sales, warehousing and the distribution to the retailers and consumers.

· Taxes on beer sales as well as business licenses

· Corporation fees that is charged on the corporations within the state as per Act 99-665 of 2002

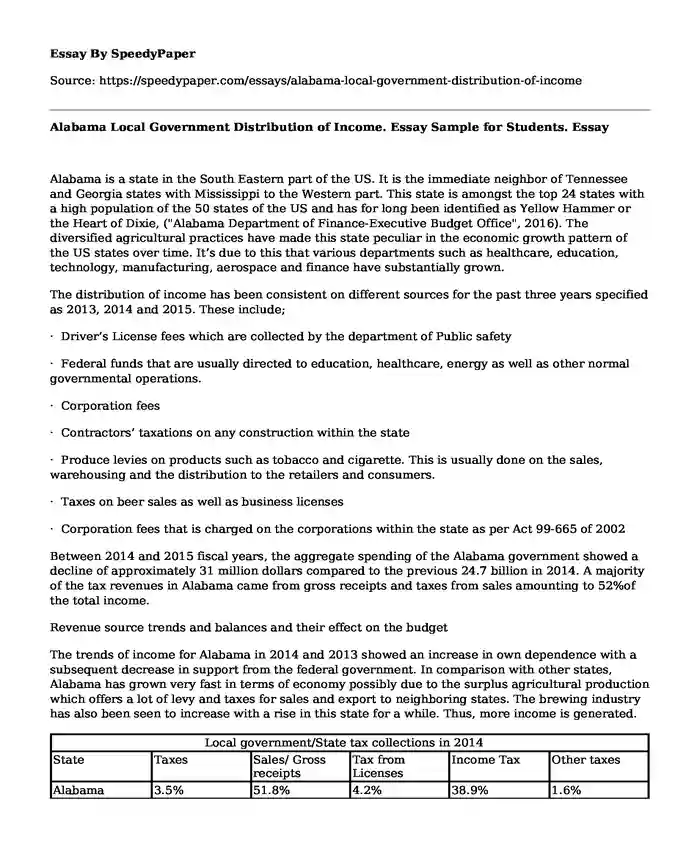

Between 2014 and 2015 fiscal years, the aggregate spending of the Alabama government showed a decline of approximately 31 million dollars compared to the previous 24.7 billion in 2014. A majority of the tax revenues in Alabama came from gross receipts and taxes from sales amounting to 52%of the total income.

Revenue source trends and balances and their effect on the budget

The trends of income for Alabama in 2014 and 2013 showed an increase in own dependence with a subsequent decrease in support from the federal government. In comparison with other states, Alabama has grown very fast in terms of economy possibly due to the surplus agricultural production which offers a lot of levy and taxes for sales and export to neighboring states. The brewing industry has also been seen to increase with a rise in this state for a while. Thus, more income is generated.

| Local government/State tax collections in 2014 | |||||

| State | Taxes | Sales/ Gross receipts | Tax from Licenses | Income Tax | Other taxes |

| Alabama | 3.5% | 51.8% | 4.2% | 38.9% | 1.6% |

| Florida | 0.0% | 82.1% | 6.0% | 5.8% | 6.1% |

| Georgia | 4.2% | 39.2% | 3.3% | 53.2% | 0.1% |

| Mississippi | 0.3% | 62.1% | 7.4% | 29.0% | 1.2% |

| Tennessee | N/A | 74.2% | 11.3% | 12.0% | 2.5% |

Source: US census Bureau

The spending despite the taxation was also low in the State thus it called for a lower support scheme from the Central government in 2015.

| The total estimates of state spending in 2015 | |||||

| State | State Fund ($) | Federal funds ($) | Total spending ($) | population | Per Capita Spending ($) |

| Alabama | 14,990 | 9,556 | 24,546 | 4,858,979 | 5,051.68 |

| Florida | 50,003 | 25,492 | 75,495 | 20,271,272 | 3,724.24 |

| Georgia | 30,593 | 12,901 | 43,594 | 10,214,860 | 4,257.91 |

| Mississippi | 11,481 | 8,953 | 20,434 | 2,992,333 | 6,828.79 |

| Tennessee | 18,806 | 13,156 | 31,962 | 6,600,299 | 4,842.51 |

Source: US census Bureau,

From the above data, the governmental inputs to this state were quite minimized due to the spending ration of the state as compared to the rest. This, in turn, does impact low governmental budgets due to the reasonable spending plans by the financial sector.

Ethical Applications of financial policies on taxes, fees, and charges

The legislators of any taxation measure have the duty to set values that are quite friendly to the taxpayers. All that does not oppress the taxpayer is what is to be legislated. For the legislation to be identified as friendly to the subjects, it has to be redrafted a number of times to ensure its genuineness and no misunderstanding, (Hemels, n.d.).

Taxation authorities do not have any right to overcharge the taxpayer. These involve the personnel on the ground that may sometimes change the taxation rates while off-office. Tax evasion is a crime as the victims are robbing the other taxpayers who take up the load, (Malm & Kant, 2016). It is an ethical responsibility of the taxpayer to comply with the taxation rates set by the authorities. With this in regard, they should not pay less than the set amount or too much than required.

Internal /external prospects and encounters of revenue sources

Internal and external opportunities

These include video advertising, Ad Networks that involve an advertising platform on different networks, E-commerce methods, paid contents in newspapers, mobile advertisements, weekly/monthly print editions as well as events hosting and promotions once in a while. Gift cards are part of the internal opportunities for membership in which individuals purchase more thus making more in terms of levies.

Internal and external challenges

Lack of transparency in amongst the collection and audit staff and some personnel in the financial analysis departments usually leads to embezzlement of funds, (Roedler, 2016). The low corporate taxes, rents and carried interests reduce the potential of the taxation development value.

There may be high dominant levels of corruption among the members of the tax collection and accountability departments. These people may collude with the taxpayers to avoid tax payment on accrued personal benefits.

References

Alabama Department of Finance-Executive Budget Office. (2016). Budget.alabama.gov. Retrieved 4 September 2016, from http://budget.alabama.gov/pages/revsource.aspx

Hemels, S. Fairness and Taxation in a Globalized World. SSRN Electronic Journal. http://dx.doi.org/10.2139/ssrn.2570750

Malm, L. & Kant, E. (2016). The Sources of State and Local Tax Revenues. Tax Foundation. Retrieved 4 September 2016, from http://taxfoundation.org/article/sources-state-and-local-tax-revenues

Roedler, F. (2016). Ifac.org. Retrieved 4 September 2016, from https://www.ifac.org/global-knowledge-gateway/viewpoints/fairness-taxation

Cite this page

Alabama Local Government Distribution of Income. Essay Sample for Students.. (2017, Oct 06). Retrieved from https://speedypaper.com/essays/alabama-local-government-distribution-of-income

Request Removal

If you are the original author of this essay and no longer wish to have it published on the SpeedyPaper website, please click below to request its removal:

- Free Essay with a Biology Graduate School Personal Statement Sample

- Free Essay: Porsche Case Study Analysis

- Free Essay: Webgraph Analysis and Webometrics - Enhancing the Structure of Academic Websites

- Literature Review Example on Success Rate of Startups in India

- Essay Example on Government Privilege and Immunity

- Essay Example on Dulles' Theology of Revelation

- Essay Sample on Employee Assistance Programs

Popular categories